Think about it: you’ve saved most of your adult life for a $3,000 Chanel Classic Flap. By 2025, you were finally ready—only to find that same bag had blown past five figures and slipped out of reach again. With Hermès pricing Birkins like compact cars and bare Louis Vuitton canvas ready to cost you as much as a small loan, your coveted dream bag remains just that—a dream.

In 2025, these hikes felt like corporate greed on steroids—but a closer look revealed a calculated pivot. Luxury houses weren’t just covering rising material costs or adjusting for inflation—they were redrawing the velvet rope. By turning aspirational treats into ultra-exclusive assets, they preserve cachet while inflating margins. That felt like a well-thought-out financial strategy.

Only this time, something feels genuinely different.

Boutiques aren’t as packed. Waitlists aren’t moving faster. And headlines are no longer screaming record-breaking growth. Instead, they’re telling a more complicated story—one where prices keep rising, but demand isn’t keeping up the way it used to.

Welcome to luxury in 2026.

Recent results from Hermès capture this shift perfectly. The brand reported just 5.6% growth in Q1 2026—missing expectations—after an abrupt slowdown linked to geopolitical tensions and declining global tourism. Sales in key luxury regions softened, and yet… prices didn’t budge.

Because here’s the truth:

Luxury price hikes were never just about demand. They were always about control.

First, Why the Price Hikes Still Haven’t Stopped

1. 2025 Was the Year of Tariffs—And the Effects Are Still Unfolding

Trade policies triggered a structural reset in pricing that brands have shown no interest in reversing:

- U.S.–China Phase II Leather Duties (January 2025). An extra 10 % tariff on finished leather goods and watch components entering the United States.

- EU Carbon Border Adjustment (CBAM) Pilot (phased‑in from Q2 2025). Luxury items with exotic skins, precious‑metal casings, or high CO₂ footprints now face a reporting‑plus‑fee regime that will add ~2–3 % to landed cost.

- Retaliatory GST Surcharges in Australia ( July 2025). A 5 % luxury‑goods levy on items over AUD 3,000, a direct answer to Europe’s CBAM rules.

Hermès, Chanel, and Louis Vuitton explicitly said: “We’re passing it on.”

What happened next:

- Permanent MSRP (Manufacturer’s Suggested Retail Price) resets, prices never came back down.

- Resale ceilings lifted almost immediately

- Supply chains shifted to tariff‑neutral countries (Vietnam for leather small goods, Switzerland for watch assembly)—but savings stayed with brands

- Regional pricing gaps narrowed to prevent arbitrage. The historical 20–25 % spread between Paris and New York tags shrunk to single digits as Europe raised prices to CBAM‑proof margins and the U.S. embedded tariff costs.

- Investors bought ex‑tariff stock. Inventory acquired in low‑duty zones (EU duty‑free airports, GCC malls) commands instant mark‑ups when listed on U.S.‑facing resale platforms.

Tariffs didn’t just increase costs—they quietly redefined the baseline price of luxury.

2. Global Economic Shifts: From “Aspirational” to “Ultra‑Exclusive.”

- The shrinking middle class in the West and a K‑shaped recovery mean fewer “one‑and‑done” aspirational buyers.

- Surging wealth in GCC and SE Asia lets brands replace volume with margin—fewer units, higher tickets, stronger aura.

- Demand elasticity flips: Higher prices now create demand by signaling gated membership.

Luxury has stopped flirting with the top 10 %; it openly courts the top 1 %.

3. Currency Volatility — USD / EUR / JPY

Currency swings created pricing loopholes—and brands shut them down fast.

- A strong USD made Europe a luxury shopping hotspot → brands raised EU prices

- A weak yen turned Japan into a resale goldmine → brands implemented “shadow price hikes” and purchase restrictions

Brand response? Price harmonization. Major houses like Chanel, Louis Vuitton, and Hermès have quietly raised EU retail prices by 8–12%, bringing them closer to U.S. levels. The goal is clear: kill cross-border price arbitrage, protect brand integrity, and maintain resale discipline.

Yen’s Weakness and Japan’s Shadow Price Hikes

On the flip side, Japan’s yen depreciation (trading at multi-decade lows vs the USD and RMB) has made Tokyo boutiques a grey-market goldmine—especially for Chinese daigou shoppers, who buy luxury goods overseas to resell them back home for a profit.

To counteract this, brands have resorted to:

- Shadow price hikes (in-store price adjustments without official announcements),

- Restricting bulk purchases and

- Stock segmentation (limiting high-demand styles to domestic consumers).

In essence, Japan becomes a retail fortress, protecting against resale leakage while preserving perceived scarcity in high-demand markets like China.

Luxury brands operate on global prestige, not local discounts. Currency imbalances distort that image. So when FX swings make one country “cheaper,” brands react fast to preserve pricing parity and prevent region-hopping arbitrage. It’s not just about margins—it’s about protecting the brand’s global ecosystem.

4. Inflation- Fanning the Flames of Price Hike or Just a Cover-Up

Raw material, labor, and logistics costs climbed with global inflation, and luxury houses definitely name‑check “higher input costs” in every earnings call. But the numbers don’t line up:

If inflation alone explained the hikes, you’d expect low‑single‑digit MSRP bumps, not Hermès tacking on 12 % in Europe or Chanel vaulting the Flap over € 10k.

What inflation does provide is cover.

With consumers already accustomed to paying more for everything—from groceries to airfare—luxury groups can ratchet up prices under the same headline. But their real motives are strategic:

- Signal Ultra‑Exclusivity – Higher tags create scarcity without slashing production.

- Margin Protection – Price is the only meaningful lever when volume stalls (see Kering, Burberry).

- Tariff & FX Padding – Inflation rhetoric masks geopolitical surcharges that would otherwise spark outrage.

Net‑net: Inflation sets the stage but is merely a supporting actor. The starring role belongs to brand strategy—pricing as a status‑gate, a margin guardrail, and an asset‑class amplifier.

5. Profit Desperation: 2024’s Luxury Slowdown—Price Hikes as a Last‑Resort Lifeline

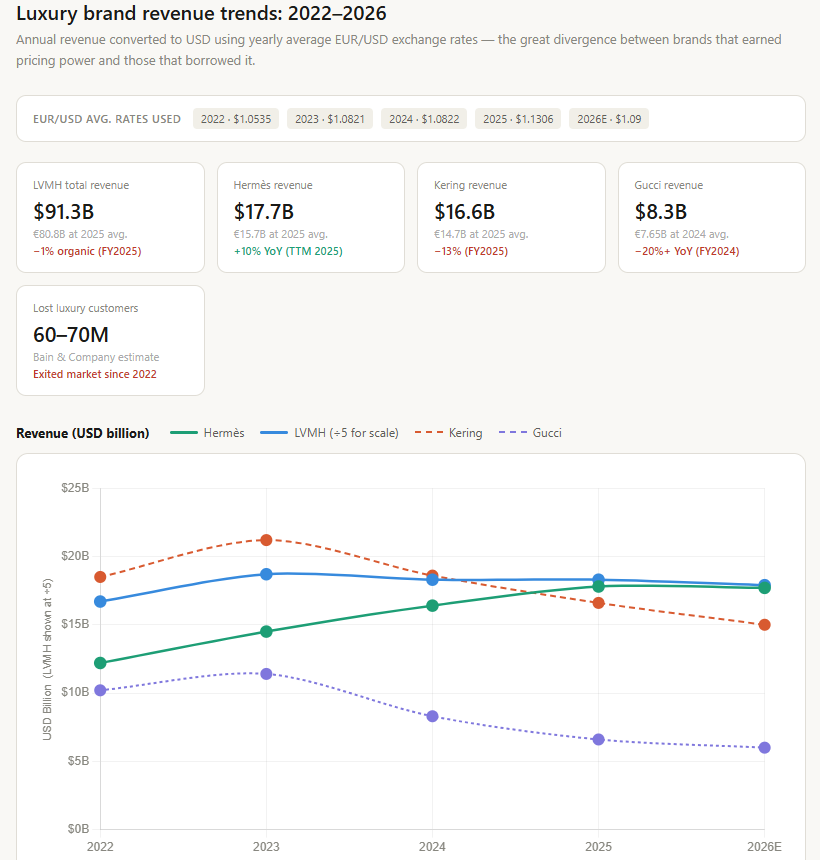

When unit growth stalls, there’s only one dial left to twist: price. That reality hit hard in 2024. Hermès was the lone titan, posting double‑digit gains—revenue up 13 % and operating profit up 17 %—and it still flexed with January and May hikes simply because it could. Richemont eked out a 4 % top‑line lift (thanks almost entirely to Cartier and Van Cleef jewelry), but wafer‑thin 2 % profit growth pushed it to “moderate” 5‑8 % price bumps across bracelets and watches. Everyone else was underwater: LVMH slipped 2 % on revenue and 5 % on operating profit, so Louis Vuitton and Dior executed 8‑10 % back-to-back increases. Kering’s Gucci‑led slump—annual sales falling 13% to €14.7 billion—forced double‑digit lifts for Gucci and Saint Laurent to protect margins. Burberry fared worst, with a 7% revenue drop and a brutal 19% margin hit; the remedy was an immediate 10% surcharge on its trench coats and signature check bags.

In short, Hermès hiked because it wanted to; the rest hiked because they had to. Because profit sagged everywhere, 2025’s big price jumps stopped being a flashy show-off move and became a must-do strategy- the quickest way to calm nervous investors and keep margins alive.

2026 Reality Check: Price Hikes Continue—But the Market Pushes Back

For the first time in years, luxury brands are facing resistance.

- Hermès missed growth expectations

- LVMH reported a 2% decline in its key fashion division

- Kering saw sales drop 8%

And the biggest disruptor?

Not inflation. Not tariffs.

👉 Geopolitics and shifting consumer behavior

What changed in 2026:

- Middle East demand weakened due to the conflict

- Tourism-driven luxury sales in Europe declined

- Airport and duty-free retail slowed significantly

- China’s recovery remained uneven

The War Effect: A Demand Shock, Not a Pricing Strategy

The Middle East conflict didn’t cause price hikes—but it exposed their limits.

- Sales in the region declined

- Dubai’s luxury retail traffic dropped sharply

- European flagship stores saw fewer tourist shoppers

- Duty-free channels took a hit

Luxury didn’t raise prices because of the war.

👉 But the war revealed what happens when high prices meet weaker demand.

In short:

👉 The volume engine is stalling

But instead of lowering prices, brands are holding the line—or pushing higher.

The Big Shift: From Pricing Power to Pricing Test

2025 was about how high prices could go.

2026 is about how much the market can take.

Luxury is now running a real-time experiment:

- Can prices rise if aspirational buyers step back?

- Can ultra-wealthy consumers sustain growth alone?

- Can scarcity still drive urgency in a slower economy?

Luxury Brands That Have Increased Prices in 2025 and Again in 2026

Luxury Brands Price Hikes in 2025 and 2026 |

|||||

|---|---|---|---|---|---|

Brand |

2025 Hike |

2026 Hike |

New Avg. Ticket |

Corporate Rationale (Justification) |

Reality Check |

| Hermès | +7 % (Jan) +5‑6 % US only (May) | +5.6% Q1 (missed targets) | Birkin 25 now ~$13,300+ | “Exceptional craftsmanship” & tariff offset | Holding the line despite geopolitical headwinds, only major brand posting growth |

| Chanel | +9 % (Mar) on Classic Flap; rumors of Q4 raise | +~10% YTD $10.2K → $11.3K | Classic Flap M/L ~$11,300 | “Global price alignment” | Reintroducing ~€500 entry items to win back aspirational buyers while flagship prices climb |

| Louis Vuitton | +4‑10 % (Apr) on canvas; +14 % exotics | “Moderate” raises for US tariffs | Neverfull MM $2.300 | “Rising costs & savoir‑faire investment” | Fashion & Leather Goods division posted –2% in Q3 2025; brand facing “quiet luxury” headwinds into 2026–27 |

| Dior (LVMH) | +8–10% back-to-back | Selective raises under J. Anderson | Lady Dior MM ~$6,500+ | “Savoir-faire & input cost recovery.” | New creative director Jonathan Anderson showing early positive signals; –2% YoY in Q1 2025 |

| Gucci (Kering) | Double-digit to protect margins | Paused — focus on creative reset | Dionysus ~$3,500+ | “Brand repositioning” | Demna Gvasalia’s “La Famiglia” collection launched Sep 2025; Kering revenue –10% in Q3 2025 vs –15% in Q2 — recovery beginning |

| Rolex | +1 % (Jan); +5 % (May) steel sports | +3–4% est. steel sports | Submariner Date ~$11,800 | “Materials & FX” | Closing gap with secondary market premiums; the grey market still commands 20–40% over retail |

| Cartier (Richemont) | +8 % jewellery, +5 % watches (Feb) | +5% est. halo pieces | Love Bracelet $8,100+ | “Metal volatility” | Richemont’s “no sharp hikes” stance contradicted by stealth bumps across Love and Juste un Clou lines |

| Burberry | +10% immediate trench & check | Holding — new CEO J. Schulman focus | Heritage Trench ~$2,800+ | “Repositioning as ultra-luxury.” | Q3 FY2026 showing improvement under Schulman’s British heritage narrative after a brutal –19% margin hit |

Note: 2026 figures reflect reported or estimated hikes as of Q1 2026. Sources: brand earnings releases, Bloomberg, WWD, Business of Fashion

Observations from the Table- Three distinct strategies emerge:

- Hermès is holding its pricing discipline (and still growing);

- Gucci has actually paused hikes to focus on its creative reset under Demna Gvasalia, and

- Brands like Chanel and Louis Vuitton are navigating the contradiction of raising prices while simultaneously reintroducing cheaper entry products to win back lost customers.

The divergence between brands that earned their pricing power and those that borrowed it is now visible in the numbers.

So, the price tags went up. What next? These aren’t just numbers on a receipt—they reshape behavior across the entire luxury food chain. Here’s what happens in the real world after the price surge:

The Waitlist Effect Intensifies — Selectively

As MSRPs soar, buyers rush to boutiques hoping to lock in old prices. With production capped, waitlists for Birkins and Classic Flaps stretch longer than ever. Scarcity becomes its own marketing machine. But the effect is no longer universal — it holds for top-tier trophy pieces while mid-tier demand quietly softens.

Sub-Brands Get Their Moment

As Chanel Flaps breach €11,000 and Hermès stretches Birkin tags to small-car territory, savvy buyers explore “next-tier” names — Loewe, Celine, Moynat — for better value. Lesser-known houses are stepping into the spotlight that the mega-brands have vacated.

Price Anchoring Rewires Perception

Once a Flap costs €11,300, a €6,000 bag suddenly feels like a deal. Strategic price hikes don’t just inflate the price of one item — they recalibrate what consumers perceive as “normal,” nudging even mid-tier buyers further upmarket. It is not an accident, but an architecture of aspiration.

Aspirational Consumers Sit Out — For Now

Those saving for a dream bag have hit pause or pivoted. Entry-tier items (LV wallets, Gucci mini bags, Chanel cardholders) absorb relative demand. Some buyers move to alternative brands — Telfar, Polène, and quiet-luxury indie ateliers — as “loud logo” fatigue spreads. Others delay.

The Resale Effect: Luxury’s Equal and Opposite Reaction

There’s a simple way to understand what’s happening to luxury in 2026: action and reaction.

The action is clear — relentless price hikes across houses like Hermès, Chanel, Louis Vuitton, and Gucci.

The reaction? A resale market that’s no longer secondary — it’s strategic.

As retail prices stretch further out of reach, pre-owned luxury doesn’t just become attractive; it becomes financially intelligent. Every boutique price increase quietly lifts the resale floor, but here’s where it gets interesting — well-curated resale platforms still offer pricing inefficiencies. Pieces sourced before hikes, or listed with competitive discounts, often sit below their true market value — creating a rare window where buyers gain both access and upside.

What was once considered “vintage” is now repositioned as value — and increasingly, value with a margin of safety.

From Smart Buying to Strategic Positioning

In 2025, resale was a savvy alternative.

In 2026, it’s becoming a necessity.

The shift is structural:

- From impulse to intent — buyers are timing purchases, not chasing drops

- From access to value — ownership matters less than entry price and upside

- From consumption to allocation — luxury is increasingly treated like an asset

A Birkin isn’t just a bag anymore — it’s a wearable store of value. But even here, the market is maturing. Early signs of softening at the very top signal something important: pricing power, even at its peak, has limits.

The New Mechanics of Value

Three forces are quietly reshaping the market:

1. Pre-hike inventory as arbitrage

Pieces sourced before recent increases immediately gain relative value. The moment a new price hits retail, older stock becomes underpriced by comparison — especially when offered at a discount on curated resale platforms.

2. Scarcity beyond production

Discontinued styles and retired materials now benefit from double scarcity — no longer made, and now benchmarked against higher current prices.

3. Global pricing inefficiencies

Inventory sourced from lower-tax regions (GCC, EU duty-free, travel retail) carries a built-in margin when resold in high-duty markets. When combined with platform-led deals and pricing strategies, this creates compelling entry points even in a rising market.

Trust Is the New Luxury Currency

As resale values rise, so does the risk of counterfeit.

Authentication is no longer a backend function — it’s the foundation of the entire ecosystem. The platforms that win won’t just sell luxury; they’ll guarantee it — while also unlocking smarter pricing through curation, condition grading, and access to pre-hike inventory.

Not a Slowdown — A Recalibration

Luxury isn’t collapsing. It’s correcting.

- From growth → selectivity

- From volume → value

- From aspiration → exclusivity

The brands that earn their pricing power — through craftsmanship, control, and genuine scarcity — will continue to pull ahead. The rest will face increasing scrutiny in a market that’s no longer willing to pay unquestioningly.

The Real Shift: Timing Over Access

The smartest buyers in 2026 aren’t the ones walking out of boutiques with the latest release.

They’re the ones who understand timing:

- Buying before the next hike

- Targeting underpriced pre-owned inventory

- Recognizing value before the market reprices it

Because today, luxury isn’t defined by ownership alone.

It’s defined by when — and how — you buy.

With boutique prices climbing and value concentrating in the secondary market, the opportunity is already out there — often quietly sitting in curated collections where pricing hasn’t fully caught up to retail inflation.

A pristine, pre-hike piece — especially one secured at a relative discount — isn’t just a purchase. It’s positioning.

And in this market, the difference between a smart buy and a missed opportunity is simply timing.

Frequently Asked Questions: Luxury Price Hikes & Buying Smart in 2026

How is the ongoing geopolitical conflict affecting luxury prices in 2026?

The Middle East conflict has weakened tourist traffic in hubs like Dubai, softening demand — but retail prices haven’t followed. Brands are deliberately holding or raising prices to protect exclusivity and margins. The disconnect between weaker demand and higher boutique tags is precisely what’s creating opportunity in the resale market right now.

Why do luxury brands like LVMH, Hermès, and Chanel keep raising prices even as sales slow?

Price is the last lever brands can pull when volume stalls. Rather than discount and dilute decades of brand equity, houses like LVMH, Kering, and Chanel prefer to sell fewer pieces at higher prices. When revenue falls — as it has for LVMH (−1%) and Kering (−13%) in 2025 — price hikes protect margins and reassure investors, even at the cost of losing aspirational buyers.

Is 2026 a good time to buy luxury bags in Dubai?

Counterintuitively, yes. Rising boutique prices, softer demand, and pre-hike inventory still available on the secondary market create a rare buying window. The gap between a retail price hike and resale prices catching up is historically short — buyers who move during that window consistently get the better deal.

Where can I find luxury bags at a discount in Dubai in 2026?

Not at boutiques — retail prices in Dubai reflect the latest global MSRP increases with no exceptions. The opportunity is in authenticated resale platforms like The Luxury Closet, where pre-hike inventory, discontinued styles, and pieces from brands under performance pressure are regularly priced below current retail benchmarks.

Which luxury categories offer the best value in Dubai right now?

Three stand out: pre-hike iconic styles (Chanel Classic Flap, Hermès Birkin) that carry built-in upside the moment the next increase lands; discontinued Louis Vuitton and Dior pieces now benchmarked against much higher current MSRPs; and select Gucci styles, where the brand’s ongoing creative reset has created temporary pricing anomalies on the secondary market.

Can I still find a pre-hike Hermès Birkin or Chanel Classic Flap in the UAE?

At the boutique, no — 2026 increases are already embedded in retail prices, with the Birkin starting at $13,300 and the Classic Flap M/L crossing $11,300. On authenticated resale platforms in the UAE, pre-hike pieces do still surface. These carry meaningful value, especially given that the next round of increases is a question of when, not if.

Is Dubai’s resale market more competitive than other markets right now?

Often, yes. Dubai sources luxury inventory from lower-tariff regions — GCC countries, EU airports, Swiss boutiques — giving local resellers a structural pricing advantage over markets like the U.S. or Australia that now carry tariff surcharges. Add current demand softness from reduced tourism, and sellers are more flexible on pricing than they’ve been in years.

Do luxury prices in Dubai ever come down after a tourism slowdown?

Never at retail. Brands respond to slower tourism by tightening supply and focusing on top-tier clients — not discounting. Price relief happens downstream, in resale, where reduced boutique footfall makes sellers more flexible and platforms more competitive. That’s where the real deals in the UAE luxury market are found right now.

Are discounted luxury bags on Dubai resale platforms authentic?

On reputable platforms, yes. A lower price reflects market conditions — pre-hike stock, motivated sellers, category softness — not a compromise on authenticity. Look for platforms that offer expert authentication, detailed condition reports, and clear return policies. Avoid unverified peer-to-peer listings, where the risk of counterfeit items is significantly higher.

What’s the smartest way to buy luxury in Dubai before the next price hike?

Four rules: buy before the hike cycle, not after. Prioritize pre-owned and pre-hike inventory over boutique stock. Focus on timeless styles — Birkin, Classic Flap, Neverfull, Love Bracelet — that hold value across brand performance cycles. And watch brands under pressure, like Gucci, where market conditions have created temporary resale anomalies that long-term valuations are likely to correct upward.

In 2026, smart luxury buying in Dubai is about capitalizing on the timing gaps created by global disruption — not chasing access at boutique prices.

Pre-hike pieces in pristine condition aren’t just rare opportunities — they’re financial ones. Explore The Luxury Closet’s curated collection of authenticated luxury before today’s smart buy becomes tomorrow’s missed opportunity.

Sources:

- fashiondive.com/news/hermes-2024-revenue-earnings/740323/

- voguebusiness.com/story/companies/lvmhs-fashion-sales-drop-5-in-q1

- lvmh.com/en/publications/lvmh-achieves-a-solid-performance-despite-an-unfavorable-global-economic-environment

- forbes.com/sites/aliciapark/2024/07/17/designer-fashion-houses-are-struggling-in-the-first-half-of-2024-heres-why/

- voguebusiness.com/story/companies/richemonts-growth-led-by-strong-jewellery-sales

- pursebop.com/louis-vuitton-europe-price-increase-2025/

- pursebop.com/hermes-q1-2025-growth-tariffs-and-a-price-increase/

- purseblog.com/hermes/hermes-price-increase-may-2025/

- hodinkee.com/articles/rolex-will-raise-us-prices-in-response-to-tariffs